All of the Risk, None of the Reward: The Troubling Reality of the TAP Privatisation

TAP Air Portugal has a long history of oscillating between state and private hands, a cycle that has often been dictated by political ideology and economic necessity.

- The Early Flirtations: After decades as a state entity, TAP was first privatised in 1953, only to be nationalised in 1975 following the Carnation Revolution.

- The 2015 "Atlantic Gateway" Era: The most significant recent attempt occurred in 2015, when the Portuguese government sold a 61% stake to the Atlantic Gateway consortium, led by David Neeleman (founder of JetBlue) and Humberto Pedrosa. This was short-lived; by 2016, a new socialist government clawed back a 50% stake to ensure public influence.

- The Pandemic Pivot: The COVID-19 pandemic served as the final blow to this hybrid model. With the airline facing collapse, the state launched a €3.2 billion bailout package approved by the European Commission, effectively re-nationalising the carrier in 2020 to prevent its demise.

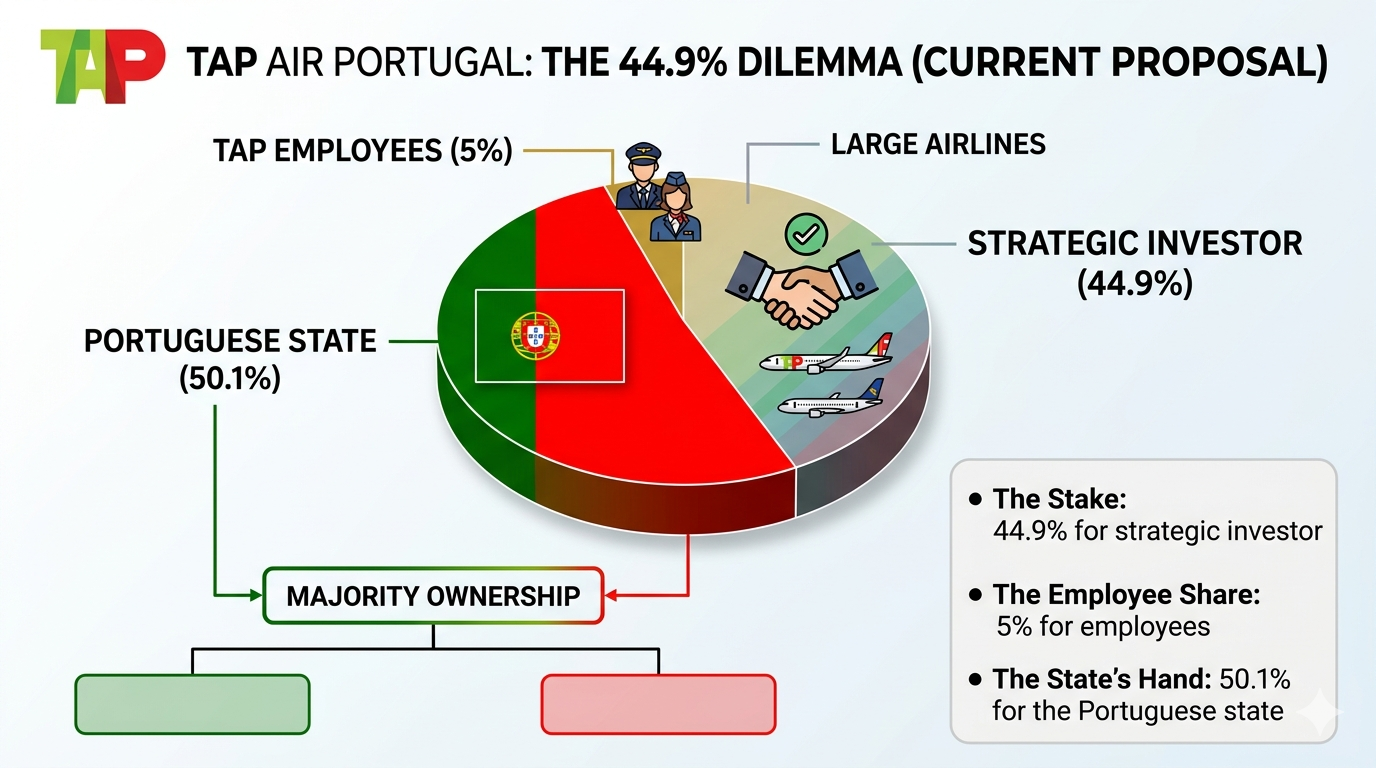

The Current Proposal: The 44.9% Dilemma

The current centre-right government has proposed a structured sale that significantly differs from the 2015 attempt.

- The Stake: The government is offering a 44.9% stake to a strategic investor.

- The Employee Share: An additional 5% is reserved for TAP employees.

- The State’s Hand: This leaves the Portuguese state with 50.1%, maintaining a majority ownership.

The Strategic Risk for Investors

As of April 2026, both Lufthansa Group and Air France-KLM have submitted non-binding bids, while IAG has cooled its interest, citing the minority stake as "inconsistent" with its strategy.

For a buyer, the risk is twofold:

- Lack of Control Rights: Without a majority stake, the acquiring group (Lufthansa or Air France-KLM) cannot fully integrate TAP into its operational ecosystem. Decisions regarding fleet procurement, hub strategy at Lisbon, and cost-cutting measures remain subject to the political whims of the Portuguese government.

- The "Veto" Problem: The government has made "safeguarding the Lisbon hub" and "national interests" non-negotiable conditions. This means an investor might provide the capital and expertise but lack the authority to steer the ship if those commercial goals conflict with Portuguese political objectives.

The Control Conundrum: Why a Minority Stake is a "No-Fly Zone" for Synergies

In the world of airline mega-mergers, the "secret sauce" is integration. When Lufthansa or Air France-KLM buys a carrier, they don't just want the planes; they want to plug that airline into their massive global machine to save costs on fuel, maintenance, and IT.

However, the Portuguese government’s current proposal—offering only a 44.9% stake—is effectively a "keep the change" deal that keeps the steering wheel firmly in the hands of the state.

For a strategic buyer, this creates a massive barrier to achieving any real merger efficiencies. Without 50.1% control, an investor cannot unilaterally make the tough calls needed to turn a profit. Instead, they are left as nothing more than a "silent partner”.

The "Political Hub" vs. The "Economic Reality"

The biggest red flag for investors is the government's mandate to maintain and expand operations at both Lisbon (LIS) and Porto (OPO).

- The Conflict: From a purely economic standpoint, a group like Air France-KLM would likely want to streamline operations.

- The Political Interference: The Portuguese state, however, views Porto as a regional priority. By forcing a buyer to expand an airport that might not fit their global network strategy, the government is essentially asking the investor to ignore market demand in favour of local votes.

Bridging the "Colonial" Gap on Private Dimes

Then there is the issue of territorial cohesion. The current proposal requires the winning bidder to maintain connections to former Portuguese colonies and autonomous regions (the Azores and Madeira).

While these routes are culturally and diplomatically vital to Lisbon, many are commercially thin or highly seasonal. In a standard acquisition, a parent company would cut these "prestige" routes to focus on high-yield transatlantic corridors. Under this deal, Lufthansa or Air France-KLM would be legally handcuffed to a network designed for 20th-century diplomacy rather than 21st-century profitability.

A Boardroom Built for Deadlock

Ultimately, the indications suggest that TAP will continue to be run to meet political goals rather than economic realities.

|

The Commercial Logic |

The Political Mandate |

|

Fleet Standardization: Moving to a single aircraft type to save on maintenance. |

Job Preservation: Maintaining local maintenance facilities even if inefficient. |

|

Network Optimization: Cutting loss-making "legacy" routes to Africa. |

National Interest: Keeping "diplomatic" routes open at all costs. |

|

Agile Management: Making quick cuts during an economic downturn. |

Bureaucratic Delay: Requiring state approval for any major strategy shift. |

For a CEO in Frankfurt or Paris, signing this deal means inheriting all the operational risks of a volatile airline while being denied the power to actually fix it. It’s a gamble where the state wins the "sovereignty" prize, and the private investor is left holding a very expensive, very restricted ticket.

The comparison to Lufthansa’s recent entry into the Italian market via ITA Airways provides a stark warning for the TAP privatisation. In the ITA deal, Lufthansa initially acquired a 41% stake—a minority position similar to what is being offered in Lisbon. However, the Italian deal included a contractually guaranteed "road to 100%," allowing Lufthansa to increase its stake to 90% and eventually full ownership once specific financial milestones were met.

The current Portuguese proposal offers no such "exit ramp" for the state. Without a legally binding mechanism to scale up to a majority, an investor like Air France-KLM or Lufthansa is effectively trapped in a permanent minority status. This lack of a clear path to total control means the buyer is essentially an "ATM with wings"—providing the capital and global brand prestige while the Portuguese government retains the ultimate "veto" over the airline's future. For a major airline group, this is the difference between a strategic acquisition and a perpetual political headache.

The IAG Factor: Disciplined Strategy vs. Political Pliability

While Lufthansa and Air France-KLM continue to flirt with the Portuguese government, IAG — the powerhouse behind British Airways and Iberia — opted to "swipe left."

A Record of Financial Rigour

To understand why IAG is hesitant, you have to look at their books. As of early 2026, IAG has solidified its reputation as arguably the best-run airline group in Europe. While its peers have struggled with fluctuating margins, IAG recently reported a record €5.02 billion operating profit for 2025, boasting a world-class operating margin of 15.1%.

Unlike its competitors, IAG operates with a "mercenary" financial discipline. They don't just collect airlines for the sake of a larger map; they demand a high Return on Invested Capital (ROIC)—which hit a staggering 18.5% in 2025. For IAG, every euro invested must yield a clear, market-driven return.

The Smart Withdrawal: Walking Away to Win

IAG’s cooling interest in TAP is a masterclass in strategic patience. In the absence of a "clear path to majority control," IAG’s leadership has signalled that they are unwilling to babysit a state-run enterprise.

- The Market Force Mandate: IAG’s business model relies on the ability to aggressively optimise its subsidiaries. If IAG can't move TAP’s back-office functions centres or adjust flight frequencies based on profitability rather than "national interest," the deal fails their stress test.

Why It Matters

By withdrawing, IAG is sending a message to Lisbon. Their reluctance exposes the central flaw in the current proposal. If the most financially successful group in Europe doesn't think the deal makes sense, it suggests that any buyer who does sign on might be prioritising political footprint over shareholder value.

IAG's skepticism isn't a sign of TAP's weakness—it's a critique of the government's restrictive terms. In a world of market forces, IAG knows that a minority stake in a politically charged environment is often just an expensive front-row seat to dysfunctional management.

Looking ahead

While TAP sits in a state of semi-integrated limbo, its competitors will not be standing still. Fully integrated groups like IAG will be able to move faster, price more aggressively, and adapt their networks in real-time. A Lufthansa-backed TAP that requires a cabinet meeting to change its catering provider or adjust its flight frequency to Luanda simply cannot compete with the ruthless efficiency of a market-driven rival.

Ultimately, by refusing to hand over the keys, the Portuguese government is ensuring that TAP remains a regional player with a global price tag. For Lufthansa or Air France-KLM, this deal may end up being less about "strategic growth" and more about a permanent subsidy for a partner they can’t control and a business they can’t fix.

For an airline group to truly unlock TAP’s potential, they need more than just a seat at the table; they need to be in the flight deck. Without that, this privatisation isn't a new beginning—it’s just the latest chapter in a long history of grounded ambitions.